Everton Financial Results: We Are Glass

Introduction:

Introduction:

In what could have been a good title for a song title by The Cure, 10:30 on a Friday Night is a very odd time for a club to tease out its financial results. Initially there was a press release, full of positives as one would expect, and enough for the media to put out a column or two.

To find out the full details it was necessary to wait though, and that’s something we don’t like because the story has become old news by the time some of the key numbers have been released (Chelsea have just done the same).

Having said that, it was a memorable season for Everton from a financial perspective, as the benefits of new owner Farhad Moshiri’s investment impacted upon both profitability and balance sheet strength. In addition, the club inched closer to a new stadium, which will be necessary financially (although will be a loss emotionally) if the club is going to break through the glass ceiling and challenge for Champions League places.

Key figures for 2016/17:

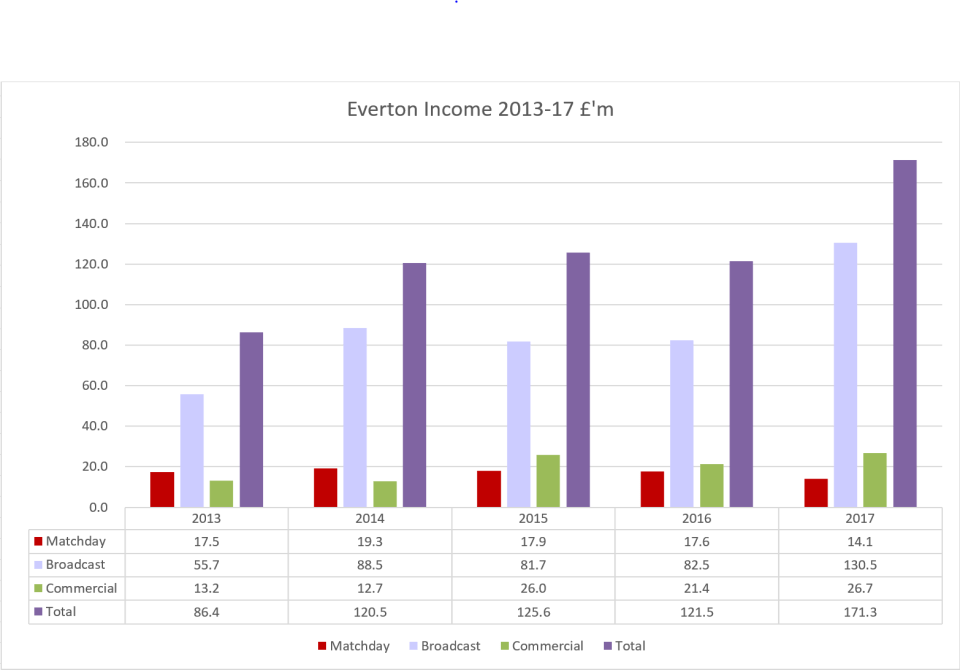

Income £171.3 million (up 40.9%).

Wages £104.7 million (up 24.6%)

Losses before player sales £12.3 million (down 28.1%)

Player signings £92.1 million

Player sales £54.7 million

Farhad Moshiri investment £150 million (£45 million since the end of the season).

League position 7th (11th)

Everton had a decent season, qualified for the Europa Cup, but were still 15 points off a Champions League place.

Everton are controlled by Blue Heaven Holdings Limited, a company based in the Isle of Man tax haven.

Bluesky are owned by Farhad Moshiri, born in Iran, his family fled the revolution and came to the UK, where he attended university in London and obtained British citizenship (no doubt being part of the migrant ‘problem’ and stealing our undergraduate places according to the Nigel Farage wing of football fans) before a successful career working for some leading accounting firms.

How he made his fortune is unclear, which didn’t stop the Grauniad having a thinly veiled pop at the nature of his investment and the role played by Alisher Usmanov, the minority shareholder in Arsenal. The inference is that Moshiri is influenced/controlled by Usmanov, but there’s no hard evidence to support that.

He then bought a share in Arsenal, before selling it to acquire 49.9% of Everton in 2016, although his loans via Bluesky make him the effective club owner.

How he made his fortune is unclear, which didn’t stop the Grauniad having a thinly veiled pop at the nature of his investment and the role played by Alisher Usmanov, the minority shareholder in Arsenal.

Moshiri also appears in the Panama Papers, which ultimately means nothing, but again fuels the nudge-nudge wink-wink school of cynic.

https://offshoreleaks.icij.org/nodes/80015954

https://www.theguardian.com/football/blog/2017/jan/25/everton-farhad-moshiri-alisher-usmanov-new-money-ownership

Income:

All clubs generate money from three sources, matchday, broadcasting and commercial.  For a club such as Everton, with no Champions League benefits and a competitive ticket pricing policy, they are reliant on broadcasting income to a greater degree than the media concocted ‘Big Six’ (ignoring that Everton have won the top division more recently than Spurs).

For a club such as Everton, with no Champions League benefits and a competitive ticket pricing policy, they are reliant on broadcasting income to a greater degree than the media concocted ‘Big Six’ (ignoring that Everton have won the top division more recently than Spurs).

After effectively treading water from an income perspective for three years, due to the Premier League (EPL) signing a TV deal of that length with BT Sport and Sky, commencing in 2013/14, Everton benefitted from the new deal that kicked in for 2016/17.

The previous season Everton had 68% of their income from TV, whilst not as much as the likes of (Plucky Little) Bournemouth, it was still substantially higher than the ‘Big Six’.

2016/17 resulted in a £48 million (58%) increase in TV revenues, most of it simply for being in the EPL, but about £8 million was due to increased prize money for finishing four places higher up the table than the previous season.

Only six clubs have reported their results to date for 2016/17, but there is a noticeable increase in the contribution made by TV monies.

Matchday income from ticket sales fell 20% to £14.1million, despite an increase in average attendances by over 1,000 to over 39,000. This was due to Everton reducing some ticket prices, especially for younger fans.

This is both a decent thing to do from an economic point of view, but also makes sense in allowing more young fans to see the club and increase the likelihood of them coming to see Everton if the move to the Bramley Moore dock stadium, where the club hope to have more than 61,000 seats available. This is dependent upon the move taking place, as costs seem to be rising all the time.

As a result, Everton’s average income per matchday fan dropped from £462 to £359. This also reflects that the club’s present facilities are not geared towards attracting large numbers of corporate fans, who pay premium prices to watch the game. Whilst there’s no love lost by regulars of any club towards the prawn sandwich brigade, the chinless wonders who occupy those seats can contribute towards the budget for players and other facilities.

A problem for Everton is the new stadium is not expected to be available until 2022. Generating about £50 million a season less than local rivals Liverpool from matchdays does put the club at a significant disadvantage if wanting to break into the Champions League contenders.

https://www.theguardian.com/football/2017/dec/31/everton-new-stadium-costs-escalate-2022-target-bramley-moore-dock

Commercial income increased by £5.3 million (24.5%). On the face of things this looks impressive, but all is perhaps not as it seems. The club signed a deal to sponsor the training ground name, which generates an impressive £6 million. This deal was signed with USM Holdings, controlled by Alisher Usmanov.

Under normal circumstances this would have Arsene Wenger’s handlers reaching for his straightjacket and the padded cell, as he would be dragged away muttering incoherently about ‘financial doping’ as he has done in the past in relation to Manchester City’s eyebrow raising commercial and naming rights deals with Etihad Airways.

It would be cynical to suggest that Wenger seems less concerned when the unusual naming rights deal comes from a major shareholder in his own club Arsenal…

Costs:

The main costs for a club are in relation to players, and come in the form of wages and player amortisation.

Wages in total rose by a quarter to £104.7 million. Only a third of clubs have reported their details to date for 2016/17, but it does seem that Everton did invest in the squad in terms of their payments to players for the season. What is noticeable is that in 2015/16 Everton’s wage bill was only 2% higher than that of Stoke, in 2016/17 this gap had increased to 23%.

This suggests that Moshiri’s commitment had found its way to the player budget, but the extra income generated ensured that that wages as a proportion of revenues actually fell to 61%. This compares to a Premier League average of 67% in 2015/16.

The wages increase might explain the USM sponsorship deal too. Under Premier League rules, clubs can only increase their wage bill by £7 million plus any increases in non-broadcast income plus the average gains from player sales over the last three years.

This is known as the Short-Term Cost Control (STCC) rule. (Anyone wanting to read it is welcome to look at page 116 of the Premier League 2017/18 Handbook, but I’m sure you’d rather pick your feet to be honest, it’s more enjoyable).

The aim of STCC is to prevent all the increases in TV monies going straight through to the pockets of players and agents. Instead the increase in this revenue stream will go to either fans in the form of lower ticket prices (kudos here to Everton) and/or club owners (because multi-millionaires need extra cash too).

For Everton, with a wage bill increase of £20.7 million, the STCC rules are satisfied as follows.

| £’m | |

| Annual increase allowed | 7.0 |

| Increase in sponsorship income | 5.3 |

| Decrease in matchday income | (3.5) |

| Averaged three year gain on player sales | 21.0 |

| Total | 29.8 |

Everton were therefore well within the rules for 2016/17, due to both the USM sponsorship and the sale of John Stones to Manchester City.

The other player related expense is that of player amortisation. This is the cost of signing a player spread over the length of his contract. Everton’s biggest signing in 2016/17 was Bolasie from small London club Crystal Palace for £25 million on a five-year contract. This works out as an amortisation charge of £5 million per year for five years.

In our view amortisation is a better measure of player investment than net player spend, as it smooths out individual transfers over a longer period of time, and shows the trend in terms of player investment.

The downside of focussing on player amortisation is that it ignores the impact of academy players and Bosman deals on the strength of the squad (but so does net player spend TBH) as these involve zero cost and therefore zero amortisation.

Following a previously seen trend in relation to Everton, the club broadly plateaued between 2014-16, but the new TV deal and owner investment allowed the club to commit more to player signings and therefore amortisation in 2017.

We would expect this figure to accelerate significantly in 2017/18 due to the £150 million spend on new players during summer 2017.

Directors pay

One beneficiary of the extra monies at the club is that of the highest paid director. The club does not name the individual (there is no legal requirement to do so), but our money is that Chief Executive Robert Elstone is the likely person. His salary increased from £400,000 to £588,000.

That’s clearly a significant pay rise, but in 2015/16 the average pay for an EPL chief executive was £1.4 million, so he is relatively underpaid for the job he does (and it has to be said he’s a thoroughly nice chap too).

Profits and losses:

Losses are income less costs, and were £12.3 million last season, or £236,000 a week, before taking into consideration player sales, mainly that of John Stones, of £54.7 million.

We tend to look at what is called EBIT (Earnings Before Interest and Tax) as a main profit metric, as this removes the volatility of player sales and one off expenses (for example, Everton paid out £11.3 million in 2016 to Roberto Martinez and his team when the manager was sacked, this expense is excluded from EBIT as it is non-recurring in nature).

Everton have made EBIT losses of £35.5 million over the last five years, which explains why they have sold players to balance the books. Total gains on player sales during the same period were £107 million.

There’s a case for saying that EBIT profits are too harsh, as it excluded player sales but included player acquisition costs in the form of amortisation.

It’s therefore also useful to consider EBITDA (EBIT with player amortisation and the depreciation of long term assets such as property and equipment) in addition to EBIT. This shows a healthier position for the club, which made an EBITDA profit every year.

Player trading:

2016/17 was a record year for Everton (although will be surpassed by 2017/18). The club purchased players for £92.1 million, and had sales of £54.7 million, to give a net spend of £37.4 million. Although the gross figures are higher than in previous years, the net spend is in line with that of recent years.

Everton seem to make a number of signings which are performance related. At the start of the 2017/18 season they were committed to additional payments for players, usually linked to appearances, trophies/Champions League qualification, international caps, loyalty bonuses and so on. This could cost the club £50 million if all the conditions are achieved, and we suspect that the fans would be more delighted than the finance department if those payments had to be made.

Even after selling Lukaku to Manchester United, Everton did spend a net £60.6 million on the squad in summer 2017. On top of this Wayne Rooney arrived on a free transfer, so expect a major increase in the wage bill in 2017/18.

The Owner:

Farhad Moshiri’s total investment is a mix of shares and quasi-loans. He paid £87.5 million for his 49.9% investment in 2016, but this money was to existing shareholders rather than the club itself.

His main action has been to pay off the bank loans of around £55 million, and replace them with an interest free advance of £105 million. During the summer of 2017, after the club’s year end, he advanced a further £45 million to fund player signings.

The early repayment of the bank loans was both good and bad news for Everton. The club had being paying out interest costs of £100,000 a week prior to Moshiri taking over, and this saving can therefore be invested in the playing squad. The banks did however charge a penalty fee £6.6 million for early repayment of the loans, revealing themselves to be a bunch of cockjuggling thundercunts harsh negotiators.

The club also took out a loan with a Chinese bank after the year end. Whether this is dipping the toe into the water in terms of financing the new stadium is yet to be seen.

Following Moshiri cleaning out the debts we estimate that the club is now worth £375 million, using our version of the Markham Multivariate Model. Given that the club was valued at £175 million when the takeover took place less than two years ago, plus £115 million in quasi-loans from Moshiri, it is a decent return on his original investment.

Summary

Everton are trying to be upwardly mobile as a result of new club ownership. To be realistically competitive for a Champions League place on a regular basis is unrealistic if the club continues to be based at Goodison, where the restrictions in terms of capacity and corporate income streams are an ongoing constraint.

By the time the Bramley Moor dock stadium is opened (and we’re assuming 2022 as the earliest date) Manchester United, Manchester City, Arsenal, Spurs, West Ham, (and possibly Liverpool and Chelsea) will have 60,000 plus capacity stadia too, and all will be aiming for those top four spots too. Having a large capacity stadium is no guarantee of success, just look at some of the clubs in the Championship.

Everton’s wage bill is currently less than half of the largest clubs, and it’s difficult to see how that gap will be eliminated in the short to medium term.

The Numbers